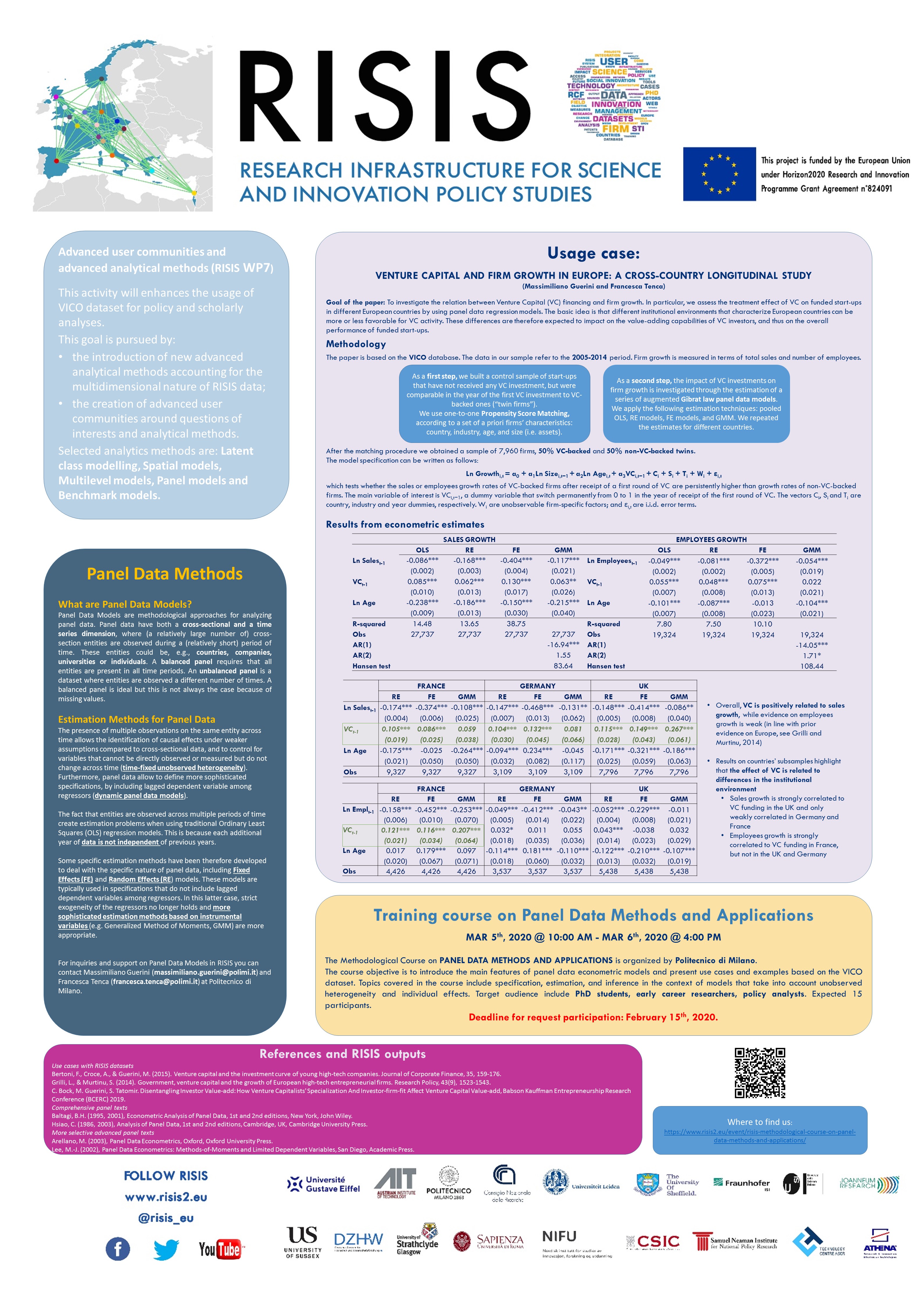

Panel Data Models are methodological approaches for analyzing panel data. Panel data have both a cross-sectional and a time series dimension, where (a relatively large number of) cross-section entities are observed during a (relatively short) period of time. These entities could be, e.g., countries, companies, universities or individuals.

Panel data allow for richer models and estimation methods than cross-sectional data. The presence of multiple observations on the same entity across time allows the identification of causal effects under weaker assumptions compared to cross-sectional data, and to control for variables that cannot be directly observed or measured but do not change across time (time-fixed unobserved heterogeneity). Furthermore, panel data allow to define more sophisticated specifications, by including lagged dependent variable among regressors (dynamic panel data models).

The fact that entities are observed across multiple periods of time create estimation problems when using traditional OLS regression. This is because each additional year of data is not independent of previous years. Some specific estimation methods have been therefore developed to deal with the specific nature of panel data, including Fixed Effects (FE), Random Effects (RE), and Generalized Method of Moments (GMM).

For inquiries and support on Panel Data Models in RISIS you can contact Massimiliano Guerini and Francesca Tenca at Politecnico di Milano.

RESOURCES

USE CASES